But during the crisis I was so focused on the financials and was so convinced that the biggest gainers coming out would be the financials that survive (and the financials seemed to be the scariest sector to even look at, which I liked) so it didn't even occur to me to look at Liberty. I did buy CBS and other stocks in other sectors and did very well with them too, so I guess it's not so much that I was only looking at financials. I don't know why, I just totally missed it. I think the Yacktman fund nailed this one.

Here is a description of Liberty Media's stock price performance from the LMC 2012 annual report (it's interesting to note that Berkshire Hathaway recently took a stake in Liberty Media. Weschler (One of BRK's new fund managers) has owned it in the past in his own fund, I think)):

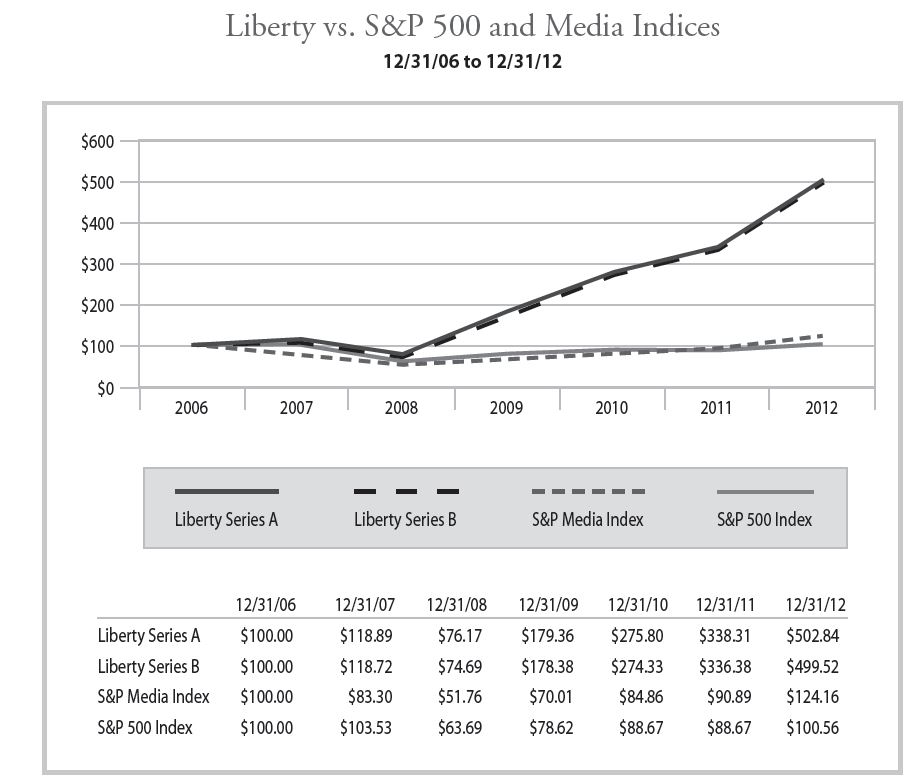

So if you invested in Liberty back in May 2006, you would have earned 33%/year through March 2013. That's an astounding rate of return no matter how you look at it. And this stock was down a ton during the crisis and I didn't buy it, knowing that it was run by one of the greatest operators of all time! That's pretty shameful.

To rub it in, let's look at a chart. This chart is from the Liberty 2012 10K:

...and this is the actual chart of Liberty Media (which spun off LMC and changed into Starz):

If you bought some stock back in early 2009, you would have had a 25-fold gain. Makes buying Bank of America look stupid in comparison; even the LEAPs.

If you even put just 10% into Liberty and 90% was held in cash (or investments that did nothing), you would have gained 36%/year since then.

Sure, there's no point in shoulda, woulda, coulda's. There are tons of those. We can't ever always get everything. I know. But this one was sitting right under my nose. I've owned it before, I've owned Discovery Communications, I've always been a fan of content and never had any doubt that content would have value (and would increase value over time as more and more people would need it), knew who John Malone was etc. There is no excuse for that.

Anyway, this would have been a career making investment (and surely it was for some; it's just that we don't hear all the stories!); kind of like Ted Weschler's W.R. Grace trade (or maybe Weschler bought a bunch in 2009!).

Next time you sit around and people are talking about finding the next subprime trade (black swan), next great bubble to short or people whining that markets are too efficient now to make the old Buffett partnership or Greenblatt-type returns, go back and look at this chart and say to yourself, "where was I and what was I doing?!"

OK, enough of that.

I may come back and take a look at Liberty and some of the other pieces of the Malone Media Complex later on.

Charter Communications (CHTR) / Malone Inteview on CNBC

But for now, what I actually wanted to do was to just post a summary of Malone's interview on CNBC not too long ago. It was an extended interview and it was fascinating for many reasons. It's not often that we get to hear a great investor talk about what he did and why he did it. In this case, David Faber of CNBC asked Malone why he invested so much in Charter Communications (CHTR).

We all know Malone built his wealth in the cable industry so it's not surprising that he is going back to it. But it is sort of surprising in that for a long time, I have looked at the content providers as where the value was in the business and the pipe-owners as not so valuable (as competition keeps increasing).

Anyway, here are some notes from that interview.

- Malone feels that 7-8x post-synergy EV/EBITDA multiple is very cheap if you can borrow at 3%. Given super-cheap capital, sustainable cash flow businesses look very attractive to be bought on leverage.

- You can't leverage a manufacturing company. Maybe you can do 2x (debt / EBITDA). But cable companies can go up to 5x leverage. CHTR will operate at 5x leverage. Malone says that's where his other companies are, Discovery, QVC etc...

- Malone believes that 80% of subscribers will reject sports programming at wholesale prices. If that is the case, the current bundling of cable channels is an unsustainable model. Cable is getting too expensive for too many households. He thinks the old model will be gone in five years.

And specifically on CHTR:

- CHTR has great management. Rutledge, by all accounts, is the best operator/manager in the business.

- Has been an undermanaged, underinvested asset for a number of years (implies potential for improvement).

- Has been a victim of a lot of market share stealing by the satellite guys.

- Faces the weakest competition terrestially. Majority of systems not in Verizon or ATT universe/areas.

- We are at a point in history where high speed connectivity is important. There is a big appetite for speed. Cable technology is the most cost-effective way to increase speed. Cable will go to gigabyte-type connectivity speed in a couple of years.

- Key is doing it cost-effectively at scale. Malone says FIOS didn't work (losing money). Overbuilding just broadband won't work.

- Malone is personally convinced that cable can get to gigabyte speed with very little incremental capital.

The other way to look at CHTR (as Malone put it):

- Great management team

- Very large tax position

- Unique position to be consolidator in the space

- debt is very cheap

- credibility of cash flow stream in cable has been growing so leverage is available

- Malone didn't want to sell; it broke his heart to sell.

- When someone offers a 40% premium you can't turn it down; responsibility to shareholders.

- In retrospect, he wishes he hadn't done it.

Back to CHTR:

- Unique opportunity to take a vehicle and grow it.

- Through both superior marketing and promotion, internal/organic growth can be exceptionally strong for a number of years.

- Particularly, the rate of growth of free cash flow can be very, very strong.

- Allows it to access leverage market in order to do rollups/transactions, particularly when there are horizontal synergies. Kind of like the old TCI model.

- Horizontal acquisitions, synergies, growth scale, opportunities to work with other cable companies to form consortia (like the old "cable mafia" as Faber said).

- Malone said he wants to bring back the old days of @Home, Ted Turner etc. Back then they were able to create national scale. Now he thinks they can create global scale.

Interesting Situation

So this is an interesting situation. Malone just bought in and is just beginning to do something here. Tom Rutledge just joined a little over a year ago. This is also a post-bankruptcy play as one of the stocks we talk about here (Oaktree) sold a big stake in CHTR to Malone. I suppose it's not so much a post-bankruptcy play anymore since it's up 3x or so since reemergence.

But the fact that it is reemergent, the stock seemed to be hated and despised (due to the leverage, view that old cable is dead etc...), they got a new CEO that is "by all accounts the best operator/manager in the business" and then the greatest investor/operator in the business just bought a giant stake (and wants to do something with it), and it has big tax loss carryforwards makes it pretty interesting.

Of course, this is also risky in that it is very leveraged. A lot of people think interest rates are going to go a lot higher and that leveraged companies will get into trouble sooner or later. This is definitely not BRK at book value or JPM at tangible book. I tend not to think that rates are going higher as I am a little biased to the deflationary side (Japan-style).

It's an interesting opportunity to get on board with some amazing people in the early stages of something, but there is risk here.

I was going to do some work on the valuation but I think so much of the value here is what Rutledge and Malone can do going forward (and the deals that will come down the pike). Otherwise, the key factor in valuation is the net operating loss, which we know Malone and Co. will figure out how to use. For other money losing operations it's hard to think NOL's will ever be realized, but when you get Malone involved, you know it will be realized sooner or later.

More Special Situations

Anyway, the stock market has come a long way since I have been sort of pounding the table on it since starting this blog in late 2011 (I loved financials, the stock market, and hated gold. Not to brag or anything... well, I hated Japan and Sony too, but I did expect a hard bounce on any weakening of the currency so it was not too surprising even though the speed and magnitude were. I'm still on the fence about Japan; every few years there is this renewed enthusiasm that seems to fade. I remember the Koizumi boom too... Maybe I will make a post about Japan some other time).

And I will keep covering and talking about the financials since I do feel comfortable talking about them. But since they may be getting into more 'normal' territory than 'cheap' (well, they are still cheap, but they've come a long way), I think I should start looking at other stuff. I do look at other stuff, but posted mostly about financials.

I always wanted to talk more about special situations here, but frankly, since late 2011, the special-est situations to me were the financials. They were great companies with great managements trading for really cheap for irrational reasons. That is less and less the case these days so I want to look around at other stuff.

Since markets are no longer so unloved as I thought it was in 2011, I will have to dig around a bit more to find stuff to write about (and invest in, even though I am still long a lot of financials).

So stay tuned!

brooklyninvestor don't feel bad, during 2008 and 2009 i was looking at GGP and LVS. i only bought GGP and miss out on LVS.

ReplyDeleteit happens.

Yeah, all the time. GGP was a good one. Frankly, I don't know if I would have bought it. I think I was staring at it at some point (but didn't do much work on it). LVS too, I don't know if I would have bought.

DeleteBut Liberty? Come on! How can I let that one go? lol...

Yes, it happens. This is one of those invisible but more painful errors of "omission" that Buffett talks about...

i hear ya, for me ggp and lvs was very simple. they were in trouble due to the environemtn (they couldn't rowover their debt at exactly the wrong time, but biz was healthy) so it was a binary bet and the smart thing for the lender to do was to refi (who would want to take over these 2 giant orgs?)

Deletei only end up buying ggp due to ackman being involve in a big way, there was no one like that on the lvs side, but i only put in amount that i thought i wouldn't feel bad if i lost it all, so it wasn't a lot :(

funny how i am similiar situation was you, i bought a bunch of BAC (common, warrants, options) in 2012/2011, BAC is still one of my biggest holdings along with GM (B warrant)

ReplyDeletehowever now i am having a very hard time finding obvious value. its tough out there :(

Yes, me too. I am overweight financials. I had a bunch of BRK too, but I don't like it that much up here; more index-like returns from here, I think.

DeleteSo that's why I will spend more time looking at special situations specifically; if we can't have good value on the usual valuation metrics, then I would look at things that look OK but not nominally cheap, but where there is a real catalyst for change going forward. I think there might be a bunch of those in the Malone complex and with other investors. Look for value to be realized by corporate action etc...

Hi,

ReplyDeleteThank you for the idea, will go over the details and come back with any specific questions.

Recently I've started reading again Buffet's partnership letters and it was interesting to see how from from the very first letter he writes on how he thinks the market is overvalued so he is over-weight work-outs (special situations), how he shorts and how he loans money against the work-outs as he considers it as a sure thing. I'm wondering if you see now a similar situation and that's why you are going over to special situations as well? Would be fantastic to read about some. In addition, if you could elaborate on this "having done well going into it too" (the crisis).

I'm also long financials having bought since 2010 and finding it very difficult to part ways with it now, I don't think it's an emotional reason rather that they are not expensive and seem to be on a momentum. JPM just raised dividend, WFC will follow soon, GS will blow out everyone out of the water etc.

Yes please on Japan.

Thanks!

Roy

Hi,

DeleteYes, ideally I would like to invest more like the old Buffett than the new Buffett, even though there is nothing wrong with the new Buffett. My favorite books are Klarman's "Margin of Safety" and Greenblatt's Genius book.

'Normal' stocks are perfectly fine investments at reasonable prices but really wouldn't make an interesting blog post as I have nothing to add to say, KO is a wonderful business at a reasonable price or some such.

So I actually always want special situations anyway, but it's true that when the market gets higher I want to focus more on something 'special'. The last thing I want to own is a GDP company at the mid to later stages of a bull market (I'm not saying we are there yet; I have no idea). I'd rather my holdings depend on specific actions by a company; restructuring, turnaround, or even like this CHTR which would be dependent on Malone's deal making, financial engineering and operational turnaround etc...

Anyway, I don't know if I have much to say about Japan, actually. I still don't have a great feeling at the company level even though I do think Loeb's move on Sony is very interesting. Of course I am skeptical, but you never know. I'm sure Loeb has done a lot of work so maybe something happens there (I took a small nibble).

Japan looks to me more like a macro trade, which is not something I do much.

And yes, financials are still attractive. But when I was writing about it, everyone hated financials. Even culturally, there was Occupy Wall Street so there was still popular anger against them. The prominent Wall Street analysts (Mayo, Whitney et al) hated them and saw no reason to own them. Now they seem to love them so... That alone won't make me sell out, but still...

Thanks for reading.

Like you I'm looking for some new ideas as I have too much cash after paring down my exposue to the financials somewhat recently. GLRE is still priced very reasonably but I'm not sure about their underwriting expertise. BP might be interesting, I haven't looked closely yet but it's astock that's certainly not in favour and Seth Klarman seems to like it quite a bit.

ReplyDeleteHave you ever looked at IBKR?

ReplyDeleteThanks

Ray

Hi,

DeleteI haven't taken a look at IBKR. I tend not to be a fan of these discount brokers as they tend to have the boom/bust pattern driven by stock market speculative volume. I know that IBKR's founder is well-regarded and has created a great business.

I may take a look at it at some point, but it's not a business that I am really all that interested in now...

Thanks for reading.

What do you think about LMCA itself? It doesn't trade at much of a premium to underlying assets, so you get Malone's expertise for free. Since I'm a big believer in Malone I started a modest position early this year in this stock. BTW, I also think Charter is very interesting, however I just want to leave it up to Malone to allocate capital as he sees fit.

ReplyDeleteHow about DTV? It was one of Malone's largest positions at one point (not sure about now). Berkshire seems to be a big fan of the stock.

Hi,

DeleteI may do a series on the Malone complex depending on how much I have to say about it. He is well known, and well-regarded, and there is a lot of stuff written about his various entities on the net. (But that didn't stop me from writing about BRK etc...)

So we'll see.

I like LMCA as a concept, and I am taking a look at it as BRK (Weschler) seems to have bought some recently too. A lot of the 'value' there is in SIRI, which at first glance doesn't look all that cheap. So you would have to get comfortable with that too, I suppose.

DTV is a great cash cow and BRK owns it too and I think it's a great investment just from that point of view. I haven't looked at it myself all that closely, frankly. This is actually another 'special situation'-type thing that I should be looking at and writing about. Shame on me for not doing so.

Thanks for reading and stay tuned.

Do you have any thoughts Genworth Financial? Though the price is up a lot in the past 6 months, it may have special situation potential. The new CEO's plan is to sell non-core businesses and the stock trades at a major discount to tangible book value. On the other hand, life insurance and long-term care insurance are tough businesses.

ReplyDeleteHi,

DeleteI am not that familiar with them but I know that sector is cheap. One I looked at a while ago and didn't do anything with (maybe I should look at it again) is Symetra (SYA). WTM and BRK owns them and it's trading at a steep discount to book too and it's a potential spinoff play. With WTM/BRK ownership, I can't imagine that they would let SYA not do something about their cheapness.

I think the last time I looked, I couldn't imagine what they could do to get their ROE up in this environment. I will look again but I don't know if I will see something else.

Great stuff but the next special situation to be looked at is the one just mentioned on CNBC FNM & FRE pfds.

ReplyDeleteThis blog is really informative i really had fun reading it.

ReplyDeleteI own LMCA, but feel it is overvalued. Don't CHTR and SIRI look overvalued compared to DaVita?

ReplyDeleteCHTR's growth rate is low (H1 2013/H1 2012 = 4.8%), and there are stronger bidders jumping in for TWC - i.e. Cox and Comcast. I don't see how CHTR can make much money if it overpays for TWC. If it doesn't buy TWC, how does it grow?

SIRI looks expensive on an EV/EBITDA basis, but the key is they have tons of free cash, so it is still very attractive, particularly if they keep growing (and they think they can keep growing).

DeleteCHTR is still just finishing up with their transformation. Rutledge was on CNBC the other day and he thinks there is a lot of room for CHTR to grow by increasing revenues per households passed, products sold per customer etc. Those metrics are low at CHTR because of many years of mismanagement and the resulting bankruptcy. Profits and free cash will grow to going forward.

As for TWC, Rutledge said they don't need TWC to grow; they can grow on their own, and there are other cable systems out there that they can acquire (like they just did earlier this year).

As for overpaying, I don't know. Malone is involved and he is not the type to overpay, I don't think. They will sharpen their pencils. If anyone is going to do a deal, there are few people who you want to be on the same side on as Malone...

There are other Malone entities too, Liberty Interactice and Liberty Global that you can look at too. I notice a lot of the good funds own a lot of Liberty Global and Malone did say that the 'potential' going out is going to be Europe; that's where the interesting opportunities are. I haven't done much work on those two, though...

What do you think of the valuation here for LMCA at $136/share?

DeleteHi,

DeleteI haven't updated everything (will wait for Q4 figures) but the value is probably around this area, maybe slightly higher. The value of LMCA is largely determined by the value of SIRI, which is now a consolidated sub. To get the value, I just took the Q3 book value and added the fair value difference (between market value and carrying value) of the large holdings (as of September 2013; things haven't moved too much). That would take you to $135/share, I think (using Sept 2013 shares outstd), and SIRI is up a little last year since consolidating it.

Anyway, I may post an update once the Q4 figures are out...

Why book value as metric? Don't assets and Malone deserve a premium?

ReplyDeleteGood question. I think the Malone premium, if any, would be included in the market values of the holdings since we know Malone will create value out of them. Book value in Liberty's case is pretty much cash and investments. Some holdings are equity method (so you have to adjust for market value versus carrying value) and SIRI is consolidated.

DeleteSo 'adjusted' book value is a good approximation of the value of Liberty.

The Malone premium exists in the holdings; for example, Charter went up a lot with Malone's involvement since we know he will use that as a vehicle to create some value. If that value is reflected in LMCA, there is no need to add another premium on top of that, right?

But I don't know. Maybe others would argue that there should be a premium above and beyond that too, but I tend to assume the Malone premium is already reflected in the current market values of CHTR, LYV etc...

I don't know how to value CHTR. I haven't seen Malone or anyone else put some numbers on CHTR's valuation - its always been subjective. They say capex will go down in the future, etc.etc.

ReplyDeleteThe only number I see is $750mn of synergies with TWC - seems too small.

It reminds me of biotech or financial stocks - its all hazy.

Hey KK,

ReplyDeleteI'm wondering if STRZA intrigues you at all. I know you mentioned its great performance since the spinoff in passing, but I actually just saw it pop up on Greenblatt's screen and realized it might be kinda cheap. Its also got HBO's former CEO and original content king spearheading its campaign to become more like, well, HBO. Its also getting close to that point in time where Greenblatt said in the genius book that spinoffs (or the companies that do the spinning off) become particularly attractive. Any thoughts?

Hi,

DeleteThat's a good point. It's a spinoff (or spinee) and if it's a magic formula stock, maybe it's a lollapalooza; it's a cannibal too. People tend to see LMCA and LBTYA as the Malone vehicles (also CHTR) where we can expect some serious activity going forward, but STRZA has some serious free cash flow too. So it is definitely interesting.

My initial reaction was that I didn't really have a strong view on STRZA going forward in a chord-cutting, over-the-top video world; I tend to view the STRZA channels as 'minor' channels. But this may obviously be wrong.

I will take a closer look, and may post something if I find anything interesting. If I don't make a post, that doesn't make it a bad idea, of course.

Was curious if you had any thoughts on the new spin-off, rights offering, etc.

DeleteMy thought was, wow, these guys are busy! But then Malone has been busy like this for years and things have usually turned out really well. By having different entities focus on different things is a good thing, especially for an entity like Malone that uses a lot of debt/financing.

DeleteShould probably mention that Buffett owns a good chunk of STRZA as well (Unless it was Todd or Ted, but I think it was Buffett himself).

ReplyDeleteIs there a way to see the most recent comments across all the blog posts, instead of searching by the blog and going down to the comments section? Thanks.

ReplyDeleteI have no idea. Blogger sends me an email when there is a comment posted, but for other readers, I don't know.

DeleteAbsolutely. I use netvibes (once google reader shut down). I use the free option but I remember it being a little bit hard to find as they want you to subscribe for a big dollar value.

DeleteOnce you sign up you can subscribe to new blog posts and separately to blog comments (I do both). The only problem I have is sometimes the comments don't make sense without the previous context. Someone might respond and use generic words or go off topic.

For example, this post is about Charter, but then someone asks about STRZA and someone replies today asking about kk's thoughts on the latest spinoff (this is not a bad thing, just an observation). I didn't understand and thought I missed something on Charter because I didn't know about any spinoff.

Malone and co think the purchase of TWC will generate high teens, low 20s IRR.. Interesting, given the headline price seemed "rich". Any general thoughts on the deal? The Liberty Media investor day is a masterclass, in case you missed it.

ReplyDeleteYeah, the price does seem rich, or at least a lot richer than last year (when they went after TWC). It sounds like they are being conservative on their synergies so they are probably looking at a lot more synergies than they announced. I don't doubt Malone will get value out of these transactions.

Delete